Q1 2026 Natural Rubber Market

1. Natural Rubber Market Price Review and Analysis

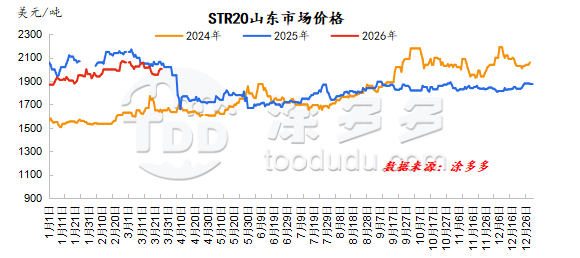

In the first quarter of 2026, natural rubber prices generally remained high and volatile. From January to February, prices generally trended upwards, primarily due to Thailand transitioning from peak production to a reduced supply period starting in January. Upstream factories replenished their inventories, and improved orders from the EU led to rising overseas raw material prices, creating strong upward pressure on costs. Meanwhile, in China, Hainan province completely ceased tapping in mid-to-late January, effectively ending China's domestic supply.

Global rubber raw material production decreased, providing strong cost support. Entering February, Thai production gradually entered its seasonal low, leading to continued increases in raw material procurement prices and processing plant costs, maintaining cost support.

The Chinese New Year holiday in mid-to-late February, followed by the resumption of work and production downstream, brought back market funds and drove up commodity prices across the board. Natural rubber followed suit, with Chinese arbitrageurs actively increasing their positions, resulting in a strong surge in natural rubber prices. Entering March, rubber prices showed a weakening trend, but remained relatively high.

Overseas producing regions gradually entered the off-season in March. Although some domestic producing areas began trial tapping, the scarcity of raw material supply in the early stages meant that domestic production could not meet the normal operating needs of local processing plants. Traders continued to rely primarily on overseas purchases.

With the continued tightening of raw material supply, overseas raw material prices also maintained a rising trend, and cost support remained strong. However, with the expectation of new domestic supply approaching, Qingdao port inventories continued their seasonal accumulation trend, maintaining a high total inventory level, which put some downward pressure on rubber prices. On the macro level, escalating geopolitical disturbances in the Middle East directly increased the cost of synthetic rubber raw materials, creating strong spillover support for natural rubber.

2. Review and Analysis of Natural Rubber Supply

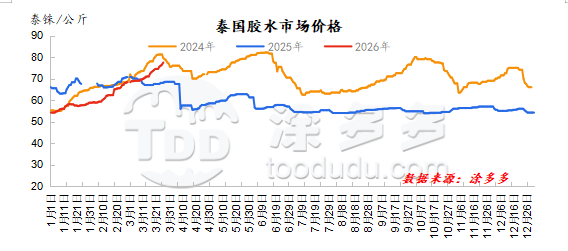

Thailand: Rubber prices maintained a steady upward trend in the first quarter, and this trend is expected to break through the high levels of the past three years. In January, rubber trees in northern Thailand began to shed their leaves, marking the end of the tapping season. Northeast Thailand is expected to maintain rubber tapping activity for the time being, with factories showing a decreasing trend in daily rubber collection. However, Thai factories have restocking needs for smoked sheet rubber, leading to a diversion of latex and a continued rise in procurement prices.

Improved demand from the EU, increased arbitrage positions in the domestic market, and improved factory orders have also driven up cup lump prices. In February, large-scale tapping ceased in northern and northeastern Thailand, resulting in strong cup lump prices. Tapping gradually ceased in the northern parts of southern Thailand, leading to a contraction in total output. Factories had restocking needs, resulting in a supply shortage of latex and a continued rise in prices.

Thai factories' raw material inventories are generally around 2-3 months, showing a downward trend compared to the same period last year, with factory shipments scheduled for August/September. In March, Thai production areas were in the seasonal off-season, leading to an extreme shortage of raw materials. Some latex processing plants raised prices to secure latex, resulting in a significant increase in latex prices and driving up raw material prices across the region month-on-month.

")

")